Ok, You now have the small amount of money it takes to buy a house. That’s the hardest part! This next step is crucial… unless you can pay cash for your property. Please note, it’s going to take 30-60 days to close on a property once you have an accepted offer, and most of this time is spent getting your loan approved with the bank.

Determining your affordability

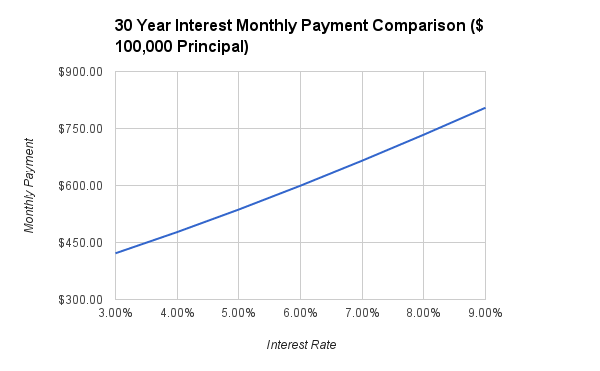

The latest interest rate I saw was at 5.5%, so for every $1000 you borrow, your principal and interest will be $5.68 at a 30 year term.

So, let’s do the math:

Don’t forget taxes and insurance (which vary for each property), and mortgage insurance.

All this can be worked backwards so you know how much home you can afford based on the maximum total monthly payment. So, if you don’t want to pay more than X dollars a month, then you can afford a Y thousand dollar home.

Choosing the lender

There are a few options out there for borrowers. Your first option is to decide whether you are going to borrow from a bank or mortgage broker. The main difference between the two is that a mortgage broker usually has a wide variety of loan programs from many different or a select few lending institutions. Where as a bank has a select set of loan programs from one lending institution; the bank they work for.

What does this mean? If you go into your local bank and ask for a mortgage, they are going to sell you a their loan. Your payments will be going to that bank. If you go to a reputable mortgage brokerage, they can shop from a wide variety of lenders to give you the best rate and terms. This also gives the mortgage broker the flexibility of finding the right program for your unique situation. Mortgage brokerages typically hire services from local small businesses like appraisers, helping the local economy, where as corporate banks typically keep everything in-house. I would recommend using a mortgage broker because they have less overhead so they tend to have lower costs, more competitive rates, are less restricted, and are more personable and understanding.

Make the call

Now you need to determine if a lender will sell you a loan based on your credit scores, household income, and other factors. Call your friendly neighborhood loan originator and ask them to pre-qualify you for a loan. This will take a few minutes of your time where they will ask you about how much you make, collect social security numbers, and the like. It is important that you answer honestly because you will have to prove everything you say when it is time to get approved for your loan. They will punch your numbers into their fancy computers and check your credit. Then they will let you know what you qualify up to and quote you a current interest rate. You could request a good faith estimate from these lenders to see their costs so you can compare to other estimates, however you will need to take some documentation and go to their office so they can accurately create one for you.

Whipple Financial Services, LLC is a great mortgage broker. Call Joe at 330-477-6762. ~~~ MB.802575.000

If you don’t qualify right away, don’t get discouraged. Whipple will work with you and point you in the right direction to be qualified ASAP at no charge.

Now, you are ready to start looking for a home, and this is where I come in. I can’t wait to show you how exciting this part is.

One thought on “First Time Home Buyer’s Guide – Part 2”